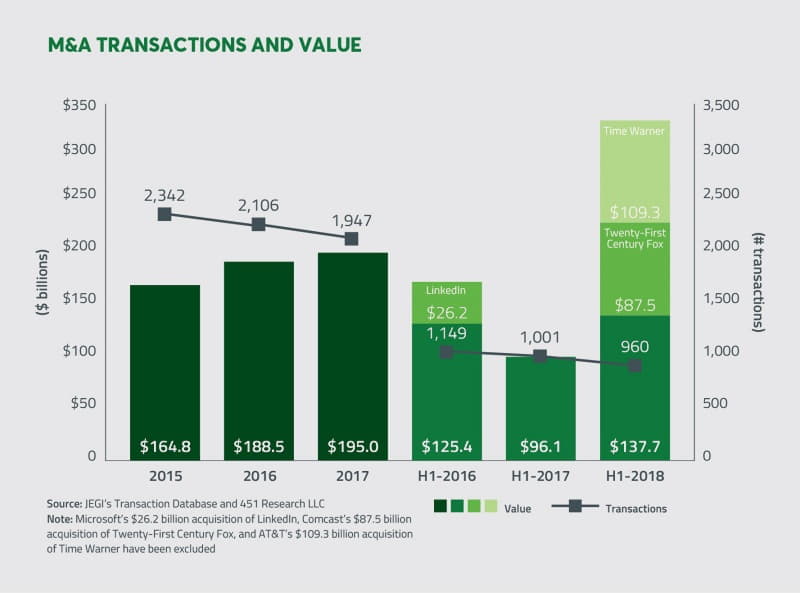

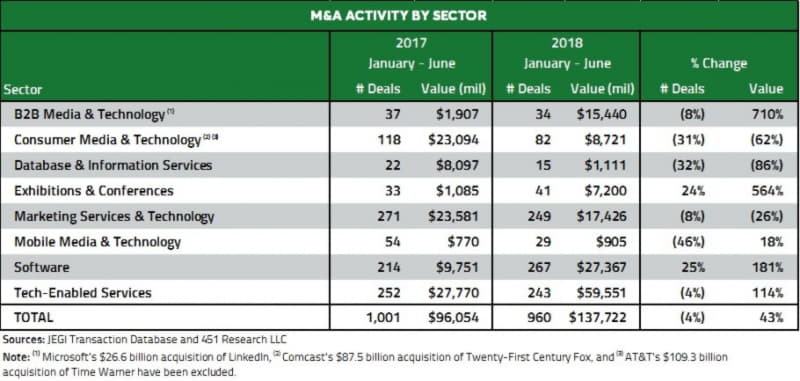

Mergers and acquisitions in the first half of 2018 across the media, information, marketing, software and tech-enabled services sectors totalled over 950 announced transactions and nearly $140 billion in aggregate transaction value (excluding the Time Warner and Twenty-First Century Fox mega-deals). Year-to-date, the pace of M&A in 2018 is on track to surpass 2016 and 2017 full-year levels.

First half 2018 transaction volume (number of transactions) declined modestly, in line with recent trends, while transaction value increased dramatically by 43% versus 2017. A notable increase in the number of large-cap transactions ($1 billion+) drove higher aggregate M&A values across substantially all JEGI sectors.

Generally speaking, H1 2017 was an “easy comp” to beat in terms of transaction value, given the extremely quiet M&A market on the heels of the 2016 presidential election. But more fundamentally, the predominance of larger transactions in H1 2018 highlights a number of powerful trends impacting buyers and sellers at the top of their sector “food chains”, trends that we expect to remain at work in the market for a sustained period of time.

To preview, those trends include:

- The corporate growth imperative

- Crossing industry lines to find new growth and profit pools

- Private Equity as an enabler of large scale reorganizations

- Relaxed anti-trust environment

- Heightened focus on consumer data security

Notable Sector Transactions and Trends in H1 2018

In B2B Media and Technology, Thomson Reuter’s divestiture of a majority stake in its largest, but low-growth Financial and Risk business unit to a consortium of investors led by Blackstone dominated H1 sector M&A value. With an implied Enterprise Value of $20 billion, the deal underscores two powerful trends at work in the marketplace: 1) the extent to which mature corporations are compelled to reorganize for future growth, and 2) the extent to which private equity firms can enable large-scale divestiture and reorganization transactions, particularly for businesses with recurring revenue and highly under-writable cash flows.

Related, Hearst Corporation’s follow-on purchase of a 20% stake in Fitch Ratings at an implied enterprise value of $14 billion, followed by Fitch’s acquisition of Fulcrum Data (a prior JEGI client) indicates the extent to which corporations are prepared to continue to cross industry lines in search of growth beyond their core markets.

In Consumer Media and Technology, the recently approved AT&T/Time Warner transaction and Comcast and Disney’son-going duel for Twenty-First Century Fox portend tectonic change in the digital media food chain. The concentration of content, distribution and advertiser/subscriber relationships resulting from these deals is formidable. And AT&T wasted no time in spending an added $2 billion to acquire AppNexus, a leading programmatic advertising platform, for deeper access to online publishers and advertisers. The Verizon/Oath transactions look timid by comparison.

While they may appear to be playing offense, the AT&T and Comcast transactions are in fact highly defensive, reflecting smart phone saturation, pricing pressure for carrier and cable services, and intensifying competition from Netflix, Amazon and others in the exploding field of streamed content. AT&T and Comcast are being forced to cross industry lines in search of growth from digital advertising. And going big. While potentially anti-competitive, AT&T’s ability to point at Google and Facebook’s +60% (and growing) share of digital ad spend made it easier for the FTC to wave the deal through — a favourable precedent for similar, future transactions.

Speaking of Facebook, transactions in the Database and Information Services sector were down dramatically versus historical and recent trends, due in part to heightened concerns over consumer data privacy. Uncertainty regarding the May 28 EU launch of GDPR (General Data Protection Regulation) has already put a damper on data transactions. Disclosures regarding misuse of Facebook data by Cambridge Analytica and others will likely weigh on sector M&A in the medium term.

Bucking the trend is the recently announced break-up of Acxiom, a take-private transaction designed to unlock the value of Acxiom’s LiveRamp on-boarding “middleware” business. Analysts believe that the sum of Acxiom’s parts well exceeds its current market value. In addition to LiveRamp, the parts include Acxiom’s legacy database marketing operations, AMS. The transaction was catalysed when Acxiom’s share price tanked in April in response to Facebook announcing its plans to cease third party data licensing. If Facebook taketh away, then Saleforce giveth: its recent acquisition of Mulesoft, a “comp” in the middleware market, places a $2+ billion value on LiveRamp. Acxiom bought the LiveRamp business in May 2014 for $310 million. Oracle, Adobe and Nielsen are rumoured buyers. And AT&T! Interpublic Group (IPG) is the confirmed buyer of Acxiom AMS for $2.3 billion (eclipsing Acxiom’s pre-announcement market cap of $2.2 billion), as IPG plays catch up with WPP/Wunderman and Dentsu/Merkle, both recognized leaders in the data-driven marketing field. Crazy that the value of a Salesforce middleware deal is driving Agency M&A.

In the broader Marketing and Technology Services sector, M&A volume and value were down slightly in H1 2018, but the category remains reliably hyperactive, reflecting on-going consolidation around specialized capabilities and select market themes. In the last 2-3 years, stiff demand for digital services — ecommerce, digital/mobile experience and cloud implementation, etc. – set off a land grab for technical talent in these fields, particularly among the consultancies and IT services firms who have rushed at the “digital transformation” opportunity. The traditional marketing services sector has been permanently altered as a result, especially at the top of the food chain where Accenture, Deloitte, IBM and PWC have emerged as the largest global digital agencies, driven by M&A. Having planted the flag, the consulting and IT firms are pushing further into digital marketing with a new focus on back-end data analytics and programmatic execution services. Get ready for the next wave of sector M&A here.

High valuations and growth rates for digital consultancies have also AT&Tracted the interest of private equity, who have a love/hate relationship with marketing services. (Talk about crossing industry lines in search of growth!). WPP’srumoured divestiture of Kantar, which has long occupied the very top of the research services food chain, will be real test of PE appetite for marketing service assets. With $4 billion in revenue, Kantar is twice as large as German research leader, Gfk, which KKR took private in H1 2017. Sizable pieces of Gfk are already in the market as part of a radical restructuring there…with a focus on pure-play data analytics.

Broad-based consolidation is also a “force at work” in the Exhibitions and Conferences sector, led by Informa’s Q1 2018 sector-redefining acquisition of UBM, its U.K. nemesis/peer, for $6.3 billion. Informa’s stock is up ~25% since the transaction was announced in January. At writing, Informa trades at 6.7X revenue and 21X EBITDA, both of which represent significant premia to…Google…highlighting the economic value of Informa’s massive, event-centric cash flows, and the durable ROI of “face-to-face” marketing. The Informa/UBM transaction represents another positive “mark” in the incredibly active Exhibitions and Conferences sector, an area where JEGI has already completed four transactions this year, including the February sale of Hargrove to Goldman Sachs’ AV services portfolio company, PSAV(on the heels of which PSAV was acquired by Blackstone in June), and the $300 million sale of Pennwell to Clarion Events (also backed by Blackstone). More M&A is expected up and down the events and conferences service chain as buyers are drawn to this attractive model and marketplace.

Software and Tech-Enabled Services

In the Software and Tech-Enabled Services sector, a few deals H1 2018 worth noting in JEGI’s core coverage categories:

- Adobe acquired Magento for $1.7 billion, a transaction that may mark the end to vigorous competition between Adobe, Oracle and Salesforce to acquire and assemble the leading commerce and marketing cloud assets.

- Microsoft acquired GitHub, a developer-focused collaboration platform, for $7.5 billion, representing another push by Microsoft into social enterprise applications, with a focus on individual users and productivity, and avoiding the hyper-competitive marketing and commerce cloud space.

- IHS Markit acquired Ipreo Holdings from Goldman Sachs and Blackstone for $1.9 billion, doubling down on data, intelligence and workflow solutions for financial institutions and capital markets professionals, and pushing Financial Segment revenue over 50% (auto and natural resources data at ~25 each, for the balance). Seeking more TAM in FinTech?

- Recruit Holdings, a Japanese HCM technology and talent recruitment media company acquired Glassdoorfor $1.2 billion. $200 million invested. Stalled growth. Flat uniques. IPO unlikely. Best market timing? Right now. “Moshi Moshi” (Japanese telephone greeting). 7X Revenue.

JEGI Very Active in H1 2018

JEGI enjoyed a strong first half, with nine closings and several others moving toward completion. In Q2, we represented PennWell, an integrated B2B events and information company in its sale to Clarion Events, a portfolio company of Blackstone; Gartner’s Workforce Surveys & Analytics, a tech-enabled survey and analytics platform in its sale to ParkerGale; Jobson Healthcare Information, a multichannel marketing communications and data provider serving pharmaceutical & healthcare professionals, in its sale to Internet Brands, a portfolio company of KKR; and MSI & Morpace, two top 20 US research and CX analytics firms, in their pre-arranged merger and sale to Symphony Technology Group; and Vendome Group in the sale of their Institute for the Advancement of Behavioral Healthcare, to HMP Communications, a medical information provider backed by Susquehanna Growth Capital. Stay tuned for additional deal announcements in the coming months.

Looking Ahead

General economic conditions remain strong heading into the second half of the year. The Conference Board’s Consumer Confidence Index decreased slightly in June from May, standing currently at 126.4. Lynn Franco, the Director of Economic Indicators at The Conference Board said, “Consumers’ assessment of present-day conditions was relatively unchanged, suggesting that the level of expected economic growth remains strong…and remain high by historical standards. Similarly, the Bureau of Labor Statistics reported that total nonfarm payroll employment increased by 223,000 in May, well above consensus expectations, with the unemployment rate in the US at 3.8%, the lowest rate since April 2000.

What to Watch

- FTC anti-trust clearance on recent major deals could encourage corporations to fast-track plans for larger M&A investments. Corporate confidence and liquidity are high to begin with…

- As reported in PwC’s 2018 Mid-Year Review, U.S. corporations and investors are holding $2.4 trillion in surplus cash (based on Federal Reserve data), available for large-scale M&A to speed up portfolio transformation, which would also add to divestiture “supply”.

- 10 years after the economic crisis, are ultra-low borrowing costs coming to end?

- Private Equity firms are spending a lot of time on “cycle risk” models…

- Public equity markets remain near record highs, but with historically high levels of volatility. Trade wars and geopolitical factors are in play.