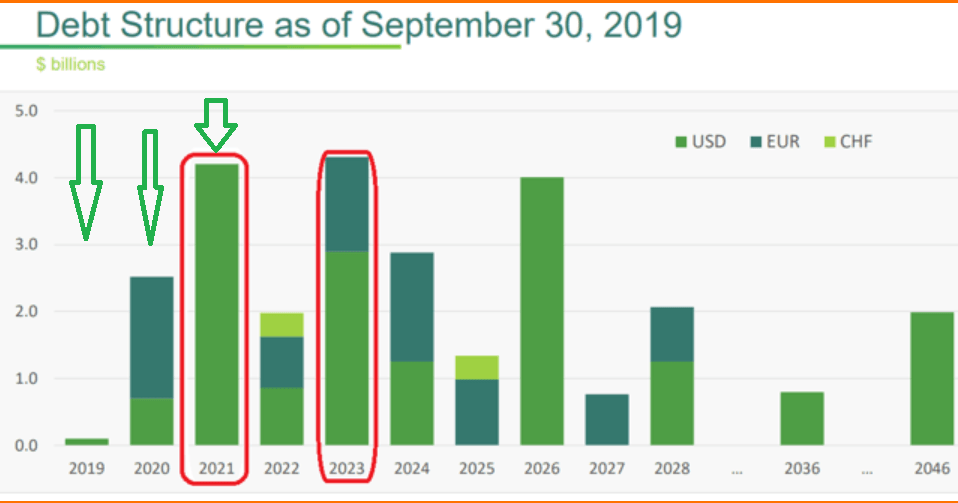

Summary

- Teva refinances all-important 2021 stack.

- Teva's turnaround is picking up momentum.

- Teva is simply too cheap now.

- Looking for more stock ideas like this one? Get them exclusively at Deep Value Returns. Get started today »

***This article was first released to readers in my Marketplace service***

Investment Thesis

Teva (NYSE:TEVA) is the biggest generics manufacturer in the world. It makes strong free cash flow and is very cheaply priced. Meanwhile, it has two significant problems:

- Debt profile.

- Overhanging opioid scandal litigation, which bearish analysts estimate to approximate $4 billion.

But I'm incredibly bullish this stock. Although I've made mistakes before and will do so again. But here is my thinking on why it may work out positively for shareholders at approximately $11 billion market cap.

(Source)

Front and Center: Debt!

Earlier this month, I wrote an article on Teva where I noted its huge debt overhang (remember, Teva has net debt of $25.7 billion and a net debt-to-EBITDA ratio of 5.62):

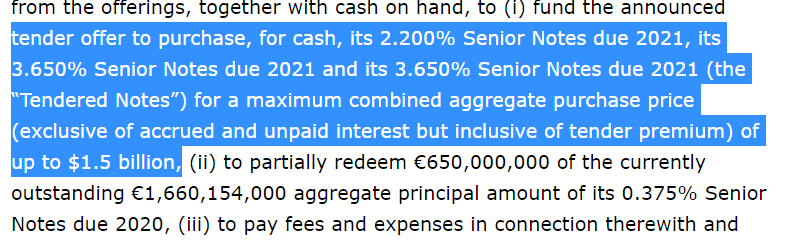

Then, less than two weeks' later, came my answer:

So, this implies that Teva is pushing back some of its 2021 stack. This is the figure I used earlier this month:

By my calculations, I believe that Teva's operations are capable of generating $2 billion of free cash flow per year.

Given that it carries $1.2 billion of cash on its balance sheet, together with this $2.1 billion debt offering, this means that its 2019, 2020, and 2021 stacks are sorted.

Thus, Teva may have problems, but let me assure you that no matter what its share price is, its debt profile is not a problem (in fact, ironically, Teva's share price actually closed the day down (!) on the back of this news)