Summary

- Citigroup is positioned to maintain profitability, despite COVID-19 presenting the ultimate stress test.

- The market is implying roughly $72 billion of after-tax losses, which seems impossible when examining Citi's loan book.

- Long-term investors can take advantage of this panicked environment to set themselves up for massive returns and dividends over the next 3-5 years.

2020 has seen one of the great panics in history on a variety of different levels. Basic common sense and rational thought have been thrown out the window, as the fear has taken over. For long-term investors, willing to go against the crowd, the opportunities are massive. Citigroup's (NYSE:C) common stock has gotten destroyed as fears of the current recession have led to memories of 2008. The company could not be more different and it very prepared to more than weather the storm and to also be a bastion of stability to its customers. Citigroup has the chance to double over 3-5 years as the fear subsides and investors once again focus on actual fundamental metrics once again.

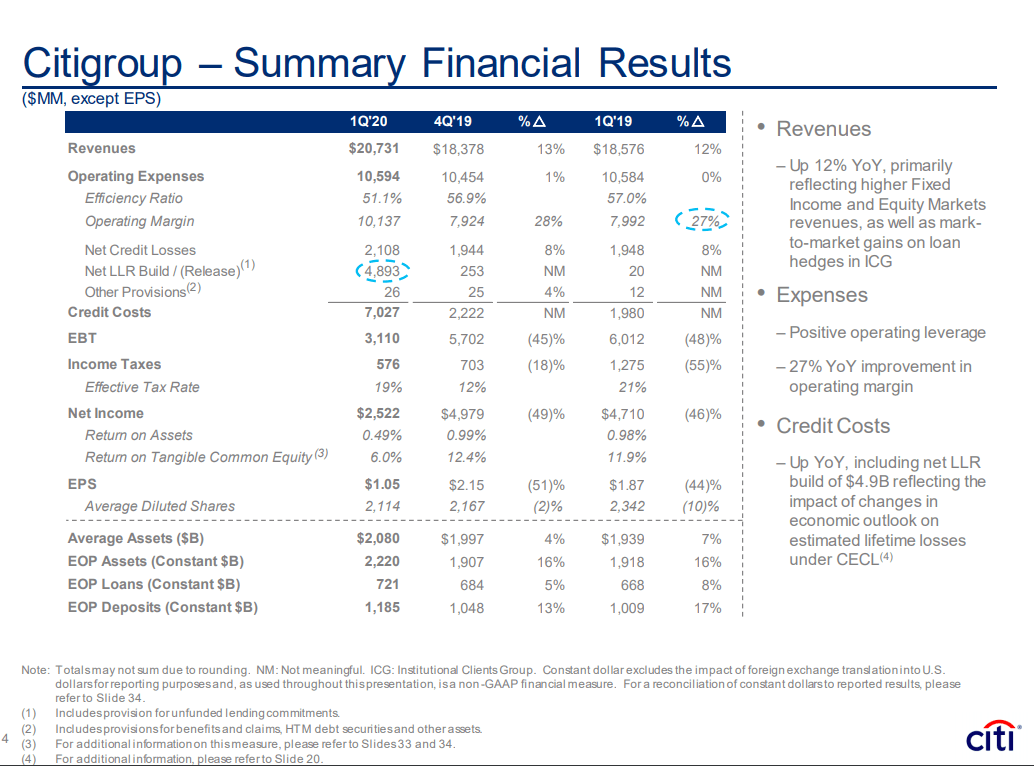

On April 15th, Citigroup reported decent earnings despite the massive COVID-19 crisis. Revenues were $20.7631 billion, up 12% YoY, and the efficiency ratio was 51.1%, which were both very strong. Citi took $2.108 billion in credit losses, while also building a reserve of $4.893 billion. Total credit costs were $7.027 billion, up from $1.98 billion a year ago. Even after all of this, Citigroup generated a net income of $2.522 billion or $1.05 on EPS. Citigroup is not as interest rate sensitive as some of its peers. In the first quarter, the net interest revenue margin was 2.48%, down from 2.63% in the fourth quarter. Net interest revenues were $11.49 billion or $10.36 billion ex-markets. Lower rates hurt but loan and deposit growth should outweigh that over time.

Citigroup ended the quarter with a Tier 1 Capital Ratio of 11.2% and a Liquidity Coverage Ratio of 115%. The SLR stood at 6%, while tangible book value per share increased 9% YoY to $71.52. The ROTCE in the quarter was 6%, which is clearly low, but very understandable given the circumstances and the reserve build. Credit reserves stand at roughly $23 billion, with a reserve ratio of 2.9% of funded loans, so Citigroup is prepared for things to get worse. The LLR for Cards is now a very healthy 9.48% and 6.1% in the GCB. We shouldn't completely discredit the fact that there are trillions of dollars in fiscal stimulus coming, and as things reopen, the economy will improve.

Some of the negative narratives around Citigroup is based on their corporate clients, but they have a high-quality loan book with significant protection and collateral. Loan losses have been very low there in the past, which was proven once again in early 2016 when oil had tanked, and many of these same concerns arose. It wasn't a problem then and it will be manageable now. The bank's massive capital and liquidity metrics, along with a very healthy pre-provision earnings power, should position the company very well to more than survive this crisis. 60% of their energy exposure is BBB or higher and we aren't talking about unsecured debt here. Many of these companies are global leaders that will most certainly survive this crisis, but, of course, everyone in just about every industry is under pressure right now.