Summary

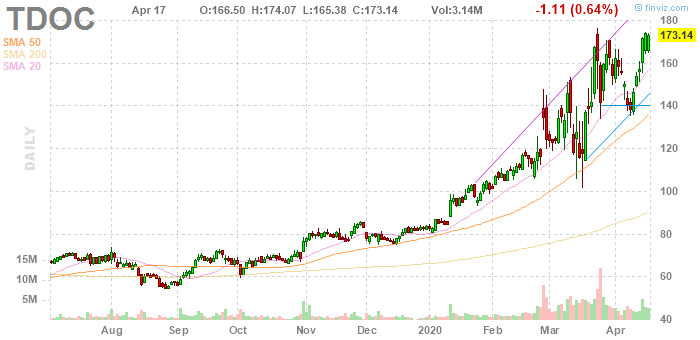

- Teladoc Health has tripled from October lows.

- The telemedicine specialist as seen a surge in visits due to COVID-19, but the Q1 results show limited benefits to the platform.

- Heading in Q2, seasonal declines in visits will hurt investor sentiment.

- The stock has an extremely stretched valuation at 17x '21 sales and over 175x '21 adjusted EBITDA.

- This idea was discussed in more depth with members of my private investing community, DIY Value Investing. Get started today »

Despite the huge surge in demand, Teladoc Health (TDOC) has seen the stock rise far in excess of the benefits of potentially one-time patients in the midst of pandemic fears. My investment thesis turned more neutral on the stock back in March and the surge above $170 is time to get out of virtual healthcare provider to conserve capital for lower prices.

Surging Demand

The telemedicine leader has already reported some impressive surges in patient visits. The average day now sees 20,000 virtual medical visits, up 100% from the start of March. By mid-March, Teladoc Health was seeing 15,000 virtual visits on peak days and 100,000 during the week.

These numbers are partly incorporated into the 70% increase in patient visits during Q1 to 1.8 million visits. Just from additional members, the company had forecast an increase of 40% during the quarter to 1.5 million total visits without a boost from COVID-19. The COVID-19 boost could reach 300K visits in the quarter.

The major hiccup to the story is the slipping app downloads. Bank of America estimated that core app downloads peaked at ~70K during the week of March 13. The downloads have now slipped to only 54K last week.

One has to wonder if social distancing doesn't end up reducing the need for other doctor visits and end up crushing demand as the COVID-19 outbreak gets under control. As doctor offices and hospitals free up space to return to normal operations, the ~60% of visits accounted for by new users to the platform could vanish.

The other issues it that surging demand isn't leading to improved economics for Teladoc Health. The company provided the following updated metrics for Q1:

- Revenue: $180-181 million

- Adjusted EBITDA: $10-11 million

With consensus revenue estimates up at $173.5 million, the telemedicine leader is only guiding to a revenue beat of $7.0 million. On top of that, Teladoc had to spend an additional $4 million on additional physician pay to cover the surging demand. The end result is EBITDA guidance mostly inline with the original Q1 guidance of $9-11 million.

Teladoc obtains over 80% of revenues from subscription access fees from members. In Q4, only $29.5 million in revenues were from visit fess. The updated Q1 guidance appears to support most of the additional visits fall into subscriptions that don't generate additional revenues.

In essence, the company saw no benefit of the jump in virtual doctor visits during the quarter. Despite being a virtual health platform, the unit economics aren't designed to benefit from one-time surges in traffic. Teladoc will need to signup new members in order for the platform to profit.