Summary

- This is a well-run regional bank, paying a near-5% dividend yield.

- While the bank will face pressures that all other major financials will face with possible loan losses in the next two quarters, non-performing assets have improved.

- The most recent earnings were rather strong, all things considered.

- Leverage weakness in share prices, and if you can get shares under $5 again, do it.

- This idea was discussed in more depth with members of my private investing community, BAD BEAT Investing. Get started today »

- Prepared by Chris, CEO Quad 7 Capital and Lead Analyst of the team at BAD BEAT Investing

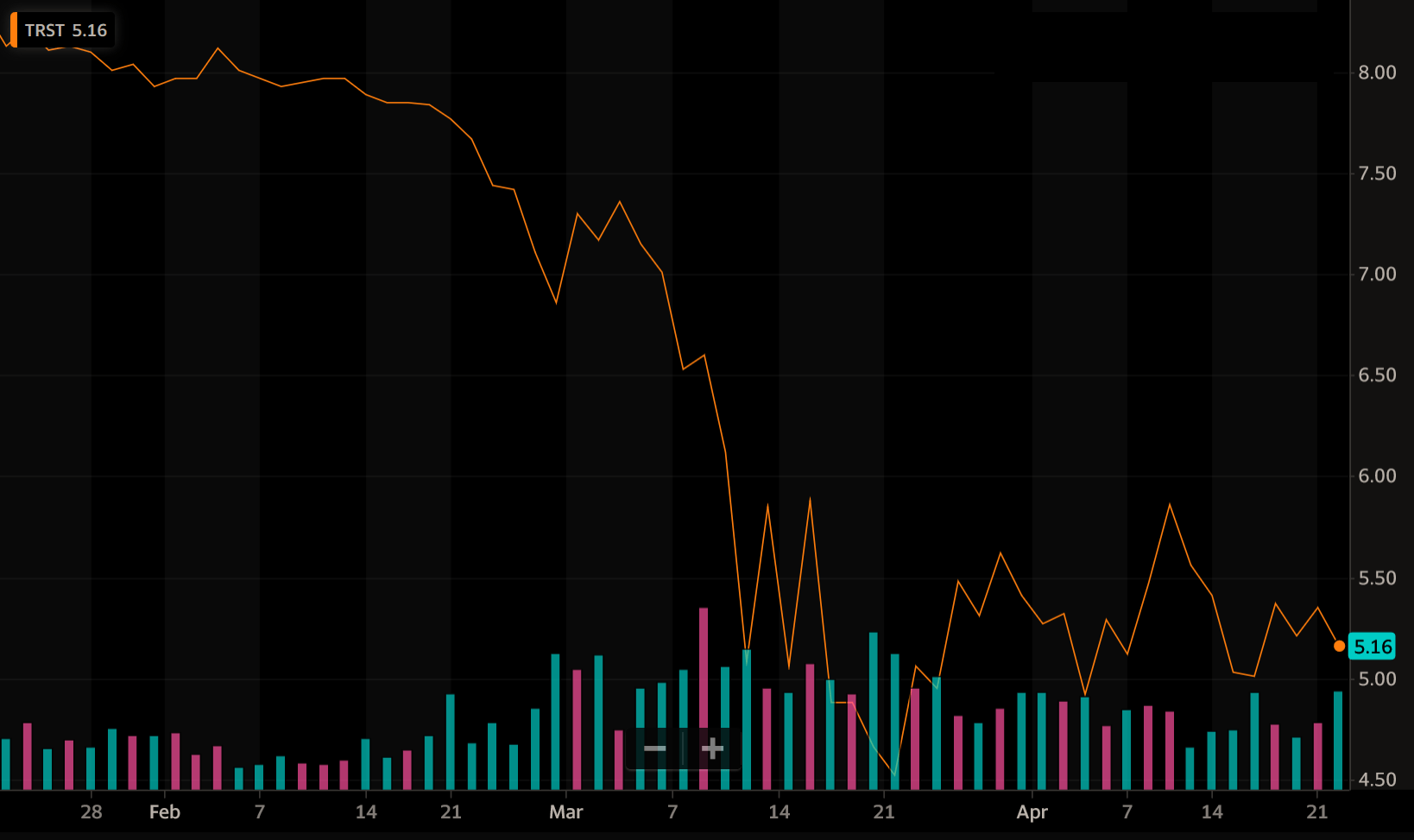

TrustCo Bank Corp. (TRST) is a name we have covered many times over the years, and have recently felt was setting up for another buy. The company just reported earnings, and the results have sparked some selling. We believe that if shares dip below $5, it is a once-in-a-decade opportunity to get into the name, in our opinion, based on valuation, the dividend, and the long-term prospects for financials. Shares retraced back to levels not seen in nearly 10 years. We are bullish on the name long term. In the near term it will be volatile, and this should be expected given the profound economic impact COVID-19 has had. Now, this bank has a lot of exposure to New York markets, and so, the market has hammered this name because there are fears it will be hit hard with the lockdown orders and the unemployment rates in New York. That said, we want to continue our coverage of this regional bank by honing on the critical metrics that investors should be focused on, and reiterate that it is a great opportunity to buy the stock.

Recent price action

The stock briefly dipped under $5 and is heading in that direction again. We think you can leverage this swing for the long-term to get into a position:

Source: BAD BEAT Investing

It is our opinion that with the stock heading toward $5.00, you should start adding to holdings here. We are definitely bullish on the name as we move forward. This is a well-run regional bank paying over a 5% dividend yield. The key metrics have some notable strengths and weaknesses to be aware of, but we think a great trade sets up here.

The play

Target entry 1 (25% of position): $5.10-5.20

Target entry 2 (35% of position): $4.80-4.90

Target entry 3 (45% of position): $4.50-4.60

Discussion

It bears repeating that unlike some major banks (think the Goldman Sachs, JPMorgans, Morgan Stanleys, etc. of the world), this regional bank is focused entirely on traditional bread-and-butter banking. What do we mean? Well, we mean that the company takes in deposits from customers at a low interest rate and makes loans to other customers at a higher rate. Bread-and-butter banking.