Summary

- Fox had an outstanding performance in Q3 and its growth prospects look promising.

- Thanks to its superior assets and a number of competitive advantages, Fox has all the chances to drive growth once the pandemic is over.

- At this stage, I believe that all the downside has already been priced into the stock and the risk of owning its shares at the current price is minimal.

Despite the rapid spread of COVID-19 inside the United States, Fox (FOX) (FOXA) has been able to show an outstanding performance in Q3 and the company is strong enough to weather the current crisis. While advertising revenue is expected to be down 25% to 35% in Q4, we should expect a swift recovery in Q1 and Q2 mostly thanks to the upcoming presidential elections that will attract new advertisers.

With P/E of 13x, Fox’s stock represents a good buying opportunity for value investors. Thanks to its superior assets and a number of competitive advantages, Fox has all the chances to drive growth once the pandemic is over. By raising $1.2 billion in debt at 3.05% and 3.5%, the company has enough liquidity to cover all of its expenses. At this stage, I believe that all the downside has already been priced into the stock and the risk of owning its shares at the current price is minimal.

No Need to Panic

I have been bullish on Fox since last year after the Murdoch family sold most of its entertainment assets to Disney (DIS) and made Fox a standalone company. While due to the pandemic my long position is currently in red territory, the company’s current share price represents a good entry point for new investors. Fox had a successful performance in Q3, as it was able to monetize the latest Super Bowl through its sports media assets. Revenues during the quarter increased by 25.1% Y/Y and were $3.44 billion. At the same time, digital advertising revenues showed impressive growth during the quarter and were up 45% Y/Y. In the first three months of the current calendar year, Fox generated more than $1.5 billion in FCF and its EBITDA was up 20%.

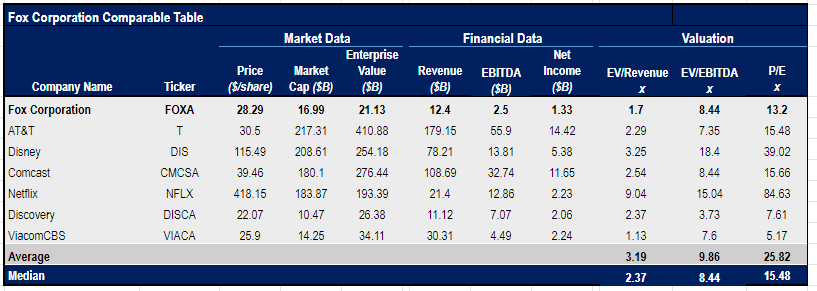

Considering this, I believe that Fox is in a strong position to weather the pandemic and create additional shareholder value along the way. With P/E of 13.2x, Fox trades below the industry’s median P/E of 15.48x and has a lot of catalysts to drive growth in the months to come.

Source: Yahoo Finance. The table was created by the author

While the company’s advertising revenues are expected to be down 25% to 30% in Q4, Fox’s shareholders shouldn’t worry too much about it. While other non-political channels will need some time to recover the lost advertising revenue, companies like Fox will only benefit from the pandemic. As we approach Presidential and Congressional elections, candidates from both sides of the aisle continue to pour more money into the TV advertising in record numbers. Despite the pandemic, the total ad spending for the current political season is expected to reach $6.7 billion, 12% more from the previous estimates of $6 billion. Since candidates cannot physically attend rallies and speak to their voters in real life, they mostly use TV ads to connect with their constituents. As CEO of Advertising Analytics Kyle Roberts said:

"These dollars can’t be allocated to the ground game right now. That does open up more dollars … that are getting appropriated to the air war."

Since Fox is the only major conservative media organization in the United States, it will greatly benefit from more ad spending in this election cycle. In May alone, Fox’s Fox News channel was able to attract 44% more prime-time viewers in comparison to the last year. The channel also became the most-watched cable network 47th month in a row. This shows that Fox’s content continues to be popular among viewers and it’s very likely that advertising revenues will recover in Q3 and Q4.