Summary

- While the Celgene acquisition added blockbusters to the company’s product portfolio, it comes with big debt and integration risk.

- Bristol’s top three drugs provide 69% of revenues.

- The patent cliffs are roughly a half decade away, the pipeline provides growth prospects, and the company’s abundant FCF should work to retire debt.

Editor's Note, July 4: A previous version of this article erroneously included commentary on Biogen's Aducanumab, which isn't relevant to BMY. The author has since deleted that portion.

My last article focused on Microsoft (MSFT), an anomaly in the universe of investments. When analyzing that company, the risk/reward profile is easily understood. There is little to fear regarding the reliability of the juggernaut's revenue streams, in the company’s projected growth, or in the firm’s financial foundation.

Consequently, one simply weighs the valuation of Microsoft to determine its viability as an investment.

This is not the case when considering the overwhelming majority of stocks. What are the growth prospects? Where does the competition lie? Is the stock nearing the top or bottom of a cycle.

The questions are myriad, the answers often opaque.

There are positives and negatives to be weighed when considering Bristol-Myers Squibb (BMY) as an investment.

The recent acquisition of Celgene juiced the company’s Q1 results, but the deal came with a heavy debt load.

Two of the company’s products, Opdivo and Revlimid, rank among the selling drugs in the world, but the company receives nearly 70% of sales through just three brands.

BMY has a robust pipeline with more than 50 compounds under development, but more than 3 dozen of the Phase 3 programs are investigating new indications for Opdivo and Yervoy, products that have long been part of the company’s portfolio

Celgene And Recent Results

To claim the company’s recent acquisition of Celgene was accretive is a gross understatement.

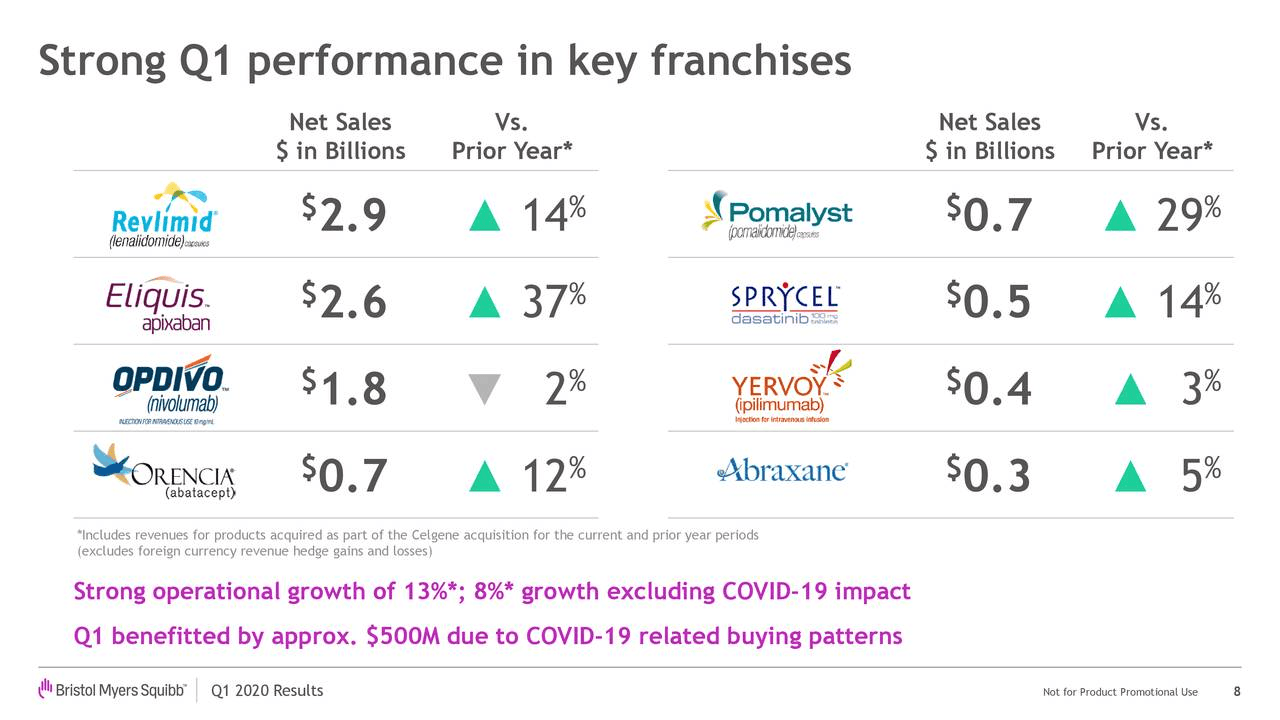

In the first quarter, revenues jumped 82% YoY, driven largely by last November’s $74 billion acquisition. On a pro forma basis, (excluding Otezla which was divested) revenue grew 13%. Of the $11 billion boost in revenues, $500 million was attributed to pandemic-related demand.

Source: Q1 Earnings Call Presentation

The deal for Celgene brought Revlimid, Pomalyst, and Abraxane into BMY's portfolio of products, and each is a blockbuster drug.