Summary

- Our diehard followers know that we said financials were going to face pressure, but there was only one that we fully endorsed.

- On the downside, we have very low rates and strong risks from loan forbearance, mortgage deferrals, and straight-up defaults.

- A big boost from traders.

- Superb efficiency.

- The best-run bank in the world.

- This idea was discussed in more depth with members of my private investing community, BAD BEAT Investing. Get started today »

Prepared by Stephanie, Analyst at BAD BEAT Investing

Those who follow our exclusive chat room frequently know that we said financials were going to face pressure, but there was only one that we fully endorsed while everyone else was negative. This was, of course, the best-of-breed JPMorgan Chase (JPM). We are frequently asked about banks, along with hundreds of other stocks a week, in our group. We have been clear - stay away from the other banks short term, but consider JPM. On the downside, we have very low rates. We also have strong risks from loan forbearance, mortgage deferrals, and straight-up defaults weighing on the sector. But we have felt the name was a good buy from $80-85. This market gave you multiple chances to get in. While real economic data weighs, the company truly put out a heroic quarter, showing why it is dominant. But it was not all good news. Relative to its competition, it was impressive. Let us discuss. We remain bullish and think it is a solid stock to not only trade but to invest in the long term, which is why we want to scale in.

Headline numbers impress

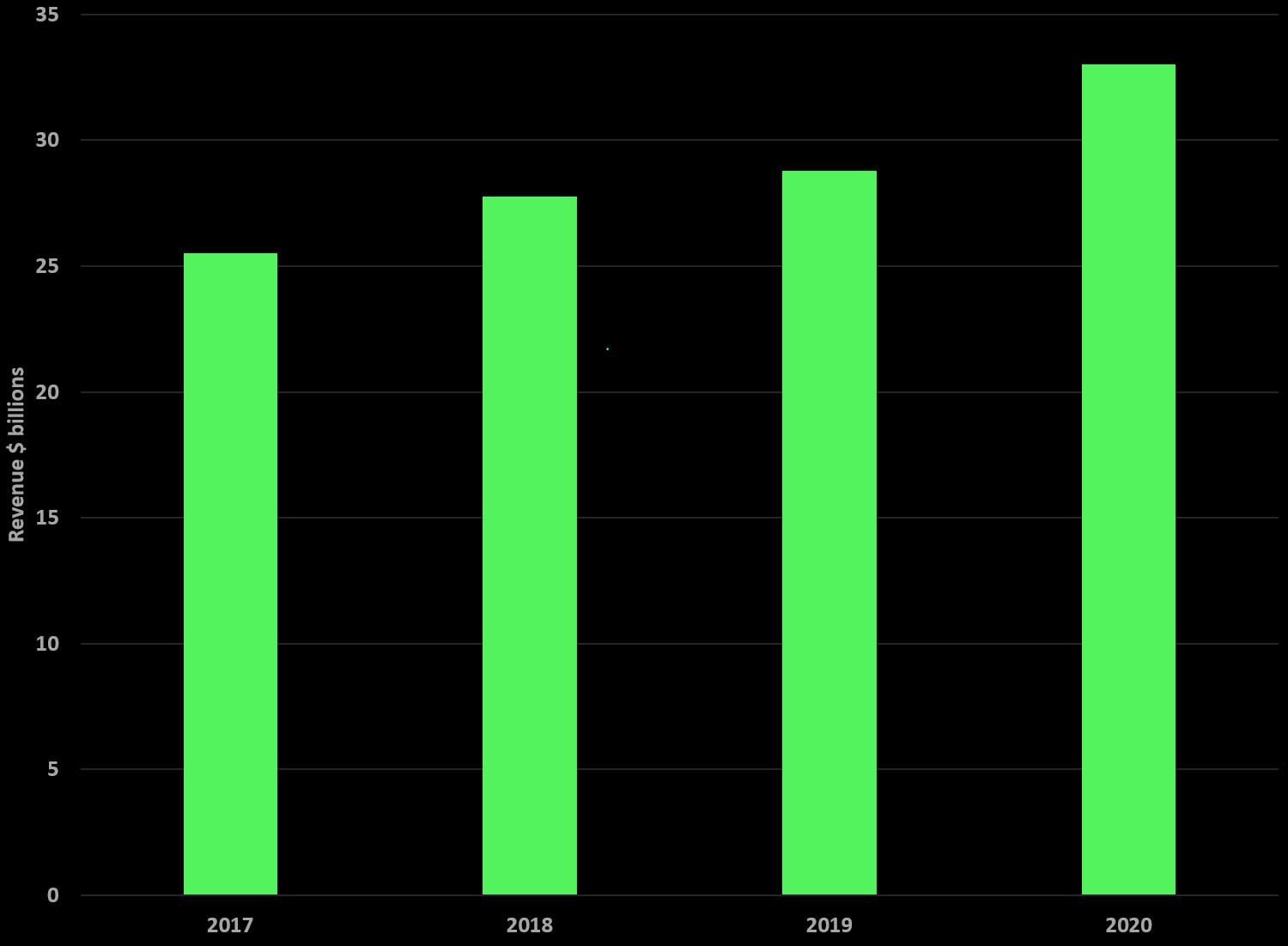

JPMorgan had a tremendous quarter when it came to the headlines versus historic performance, but relative to expectations, was heroic. No one really knew where it would come in. Overall, the headline numbers reflected the pain of the COVID-19 crisis, which has led to reduced demand and changing banking activity from the norm, but it trounced expectations. Of course, after a near-50% drop from peak to trough in the stock, well, we can see the market priced in disaster. Q2 was better than expected, but Q3 could see the pain continue, at least operationally. Managed revenue was $32.9 billion, up about 15% year over year. This was above our expectations for $30 billion by nearly $3 billion. This continues a pattern of strong growth in Q2 revenues over the last several years:

Source: SEC Filings, graphics by BAD BEAT Investing

What a result. We obviously had been ratcheting down our expectations for the year. The same thing happened with analysts. The competition has struggled. But JPM hit a home run. Revenues were eye-popping. It was not all sunshine and roses here though. Operational expenses were hiked by 4% from a year ago, while provisions for credit losses were atrocious, at a massive $10.5 billion versus an average $1.5 billion in each of the last 3 quarters of 2019. It was also up from Q1 2020's $8.2 billion. This offset the massive revenues, and EPS showed a reduction from last year's Q2: