Summary

- Citi shares have about 40% upside to book value, creating a tremendous potential value opportunity.

- The company has taken aggressive reserves, which should bolster confidence this book value level will be sustained.

- However, when normalizing for one-time factors, the company's earnings power may be a bit short of what is needed for a 1x book valuation.

- I see upside in shares, but $65 is a more realistic target.

Shares of Citigroup (C) fell nearly 4% on Tuesday as investors digested its second quarter earnings results. Interestingly, this poor share price performance came even though earnings of $0.50 beat by $0.10 on revenue of $19.77 billion, ahead by $700 million. Shares could potentially rally 40% just to return to the company’s tangible book value of $71.15 a share. Upside like that will certainly get investors excited. However, to determine whether shares can reach this level, we need to first determine whether that tangible book value figure is sustainable and whether the company can generate sufficient return on equity to merit a 1x book value valuation. On these questions, I believe the answers are yes and no.

Is Citi’s book value sustainable?

Given its worst-in-class performance among the big banks during the 2008-2009 financial crisis and long recovery since, Citigroup has always traded with a bit of a discount relative to peers. It is somewhat intangible admittedly, but there is this pervasive fear that if there is going to be a problem, Citi is bound to be exposed to it. Given over a decade has passed and management who oversaw the troubles in the financial crisis have been gone for years, it is not clear to me this discount is justified. Nonetheless, investors need to recognize that Citi’s results will face extra scrutiny, and this discount won’t disappear tomorrow.

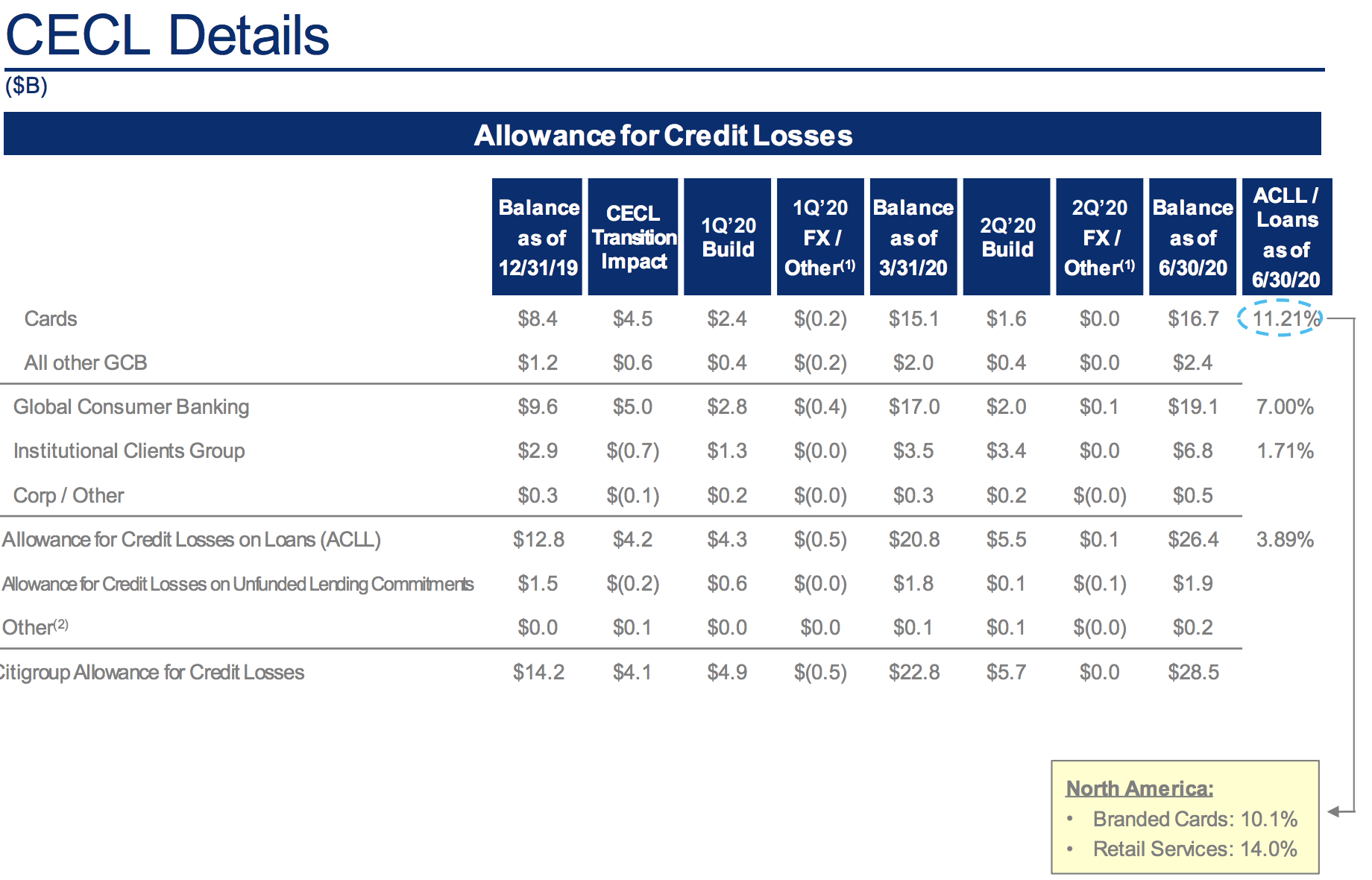

Due to this, I was pleased to see the company’s fairly aggressive reserving. During the quarter, the company set aside $5.6 billion to handle future loan losses. Loan reserves are sized to be what management expects total losses to be on the existing book of business if their economic baseline were to occur. This loss level is based on the expectation unemployment will be just below 10% at year-end, which is similar to what the Federal Reserve forecasts. Now, this forecast could prove wrong; no one knows the future, but Citi appears to be planning in a reasonable way.

Indeed, if we look at how they break down their loan reserves, Citi’s $26.4 billion of reserve against existing loans account for 3.89% of its loan book. Now, no two banks’ loan portfolios are exactly the same, but JPMorgan Chase is reserving at about 3.5% of its loan portfolio. Again, Citi’s reserve stance looks reasonable. In particular, I am heartened to see that its credit card reserves, which will be the most impacted by small shifts in unemployment relative to forecast, are 10% of loan balances in North American branded cards.

(Source: Citigroup)

On the conference call, management noted that between 40% and 60% of consumers who entered into a forbearance agreement on their Citi loan have continued making payments anyway. This suggests that the default wave one might normally associate with double-digit unemployment does not occur, in large part because fiscal stimulus measures, like enhanced unemployment benefits, have insulated incomes from job losses. Excluding forborne balances, delinquency rates on Citi’s consumer credit portfolio are only 0.9%, well below reserve levels.

All of this points me to the view that Citi has sufficiently and conservatively reserved against reasonable loss expectations. Yes, there is some art to mapping future losses to unemployment, and the outlook is uncertain, so we may or may not see small reserve builds from here. But, barring a severe second rollover in economic activity, we are unlikely to see the $4+ billion reserve hits of the past two quarters. The drag on book value from reserving is largely behind us, meaning we can view that $71 book value per share value as a sustainable estimate of Citi’s net asset position.