Summary

- Headline numbers were impressive in Q2.

- Stellar gains in investing and wealth management services.

- Loan loss provisions continue to rise, but the dividend is solid.

- While we have made solid gains, we think you can continue to buy on meaningful pullbacks.

- This idea was discussed in more depth with members of my private investing community, BAD BEAT Investing. Get started today »

- Prepared by Stephanie, Analyst at BAD BEAT Investing

Goldman Sachs (GS) is a bank we added to our coverage universe back in April, and recommended investors start buying it up when it was in the $170s. That was a solid call as the stock now trades at $215, and there is likely more room to run in the long term. Near term, it is still a terrible environment for the banks. However, the overall Q2 results appeared to be strong, justifying our buy call. In fairness, handicapping the quarter was tough. But this bank is a bit different than others in our coverage universe in that it is heavily focused on wealth and investing. Well, with the massive volatility in markets the late few months, trading and investing related revenues have skyrocketed. Although we have generated you solid returns, we still like shares at these levels and believe investors and traders can still buy on any pullback the next time the market hiccups. While the Fed and the federal government have really backstopped this market, we think you will get a chance to acquire shares for a better price. It happens. It is our opinion that overall, banking weakness will continue for a few quarters while the consumer economy is locked down, though this is temporary, while investing-related revenues should remain strong as markets are still volatile. In this column, we discuss performance and the outlook for the name.

Headline numbers

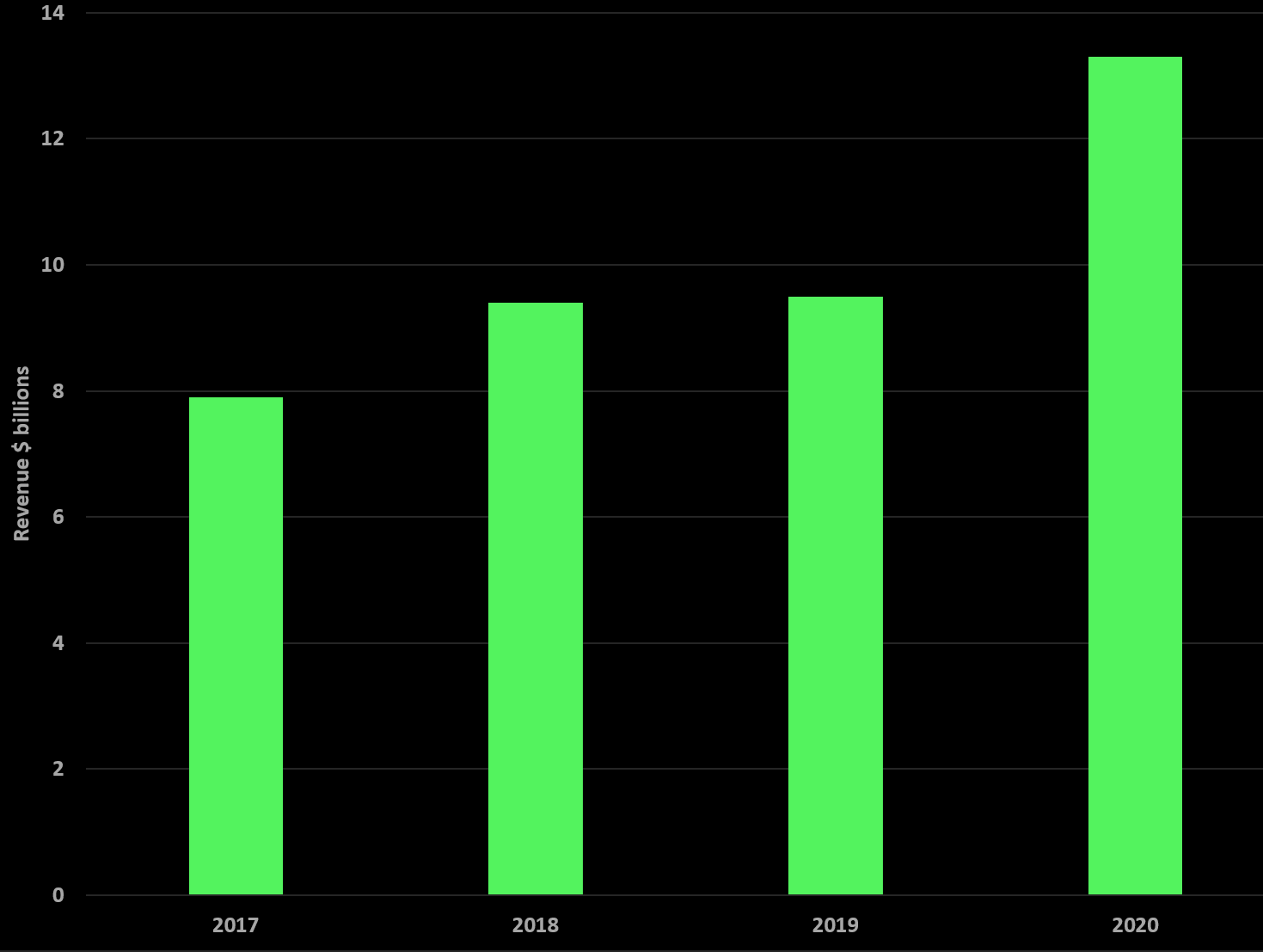

The bank reported net revenues of $13.3 billion in Q2. This was a massive increase of 40% from last year, which was well above expectations. We were looking for $10 billion, so our expectations were crushed by $3.3 billion, and continuing a solid run of Q2 top lines:

Source: SEC Filings, graphics by BAD BEAT Investing

No one really knew how it would look, and we felt we were a bit conservative in our expectations, but we never saw such a massive beat coming. Some banks missed badly. Others surprised, like Goldman did. That said, analysts' consensus was surpassed by $3.5 billion. It was also up sharply from Q1's $8.1 billion. Interestingly we thought this top line would lead to a nice result on the bottom as well.

Since revenue was up massively and way ahead of expectations, it stands to reason that earnings would be above expectations. Loan loss provisions were set very high. Operating expenses were up 37% over last year, mostly for litigation expenses and compensation/benefits. The operating environment, notably in April and May, was impacted heavily by the spread of the COVID-19 virus which caused a sharp contraction in global economic activity and increased market volatility. But that volatility drove immense trading revenues. While the huge increase in revenues was notable, the higher expenses and $1.59 billion in loan loss provisions weighed on earnings. Still, they grew. EPS came in at $6.26 per share compared with $5.81 per share last year, continuing a higher trend in recent Q2 periods: