Summary

- Analysts love Citi, expecting 48% stock price appreciation.

- However, bullish analysts underestimate the cost of Citi's latest problem.

- Expect Citi's non-interest expenses to grow faster and revenue to grow slower than peers over next two years.

- Citi is a heartbreaker and may be a value trap. Avoiding.

Analysts Love Citi

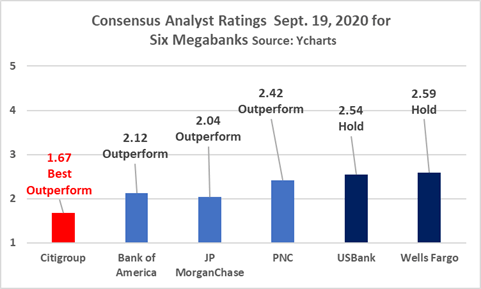

The 24 analysts who follow Citigroup Inc. (C) are bullish as Table 1 shows. No Sell recommendations. One-year price target is $67 compared to September 17 price of $44.86.

Table 1 Analyst Coverage for Citi as of 9/17/2020 (Source: YCharts)

| Consensus Recommendations | |

| Buy Recommendations | 12 |

| Outperform Recommendations | 8 |

| Hold Recommendations | 4 |

| Underperform Recommendations | 0 |

| Sell Recommendations | 0 |

| Consensus Recommendation | 1.667 |

| Consensus Rating | Outperform |

| Target Price | |

| Price | 44.86 |

| Price Target | 66.31 |

| Price Target Upside (Daily) | 47.82% |

Chart 1 shows bank analysts like Citi more than its megabank peers.

Chart 1

Citi's Low Valuation: Opportunity or Value Trap?

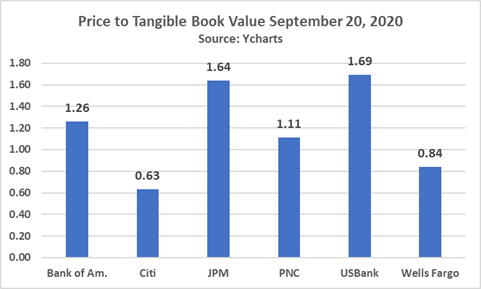

Analysts often cite Citi's low valuation as a primary reason for the bank's upside. Chart 2 shows the Price to Tangible Book Value of six big banks as of September 20.

When a bank, or any investment for that matter, has a deep discount to apparent value, investors must ask: Is the discount an opportunity or a potential value trap?

Chart 2

Risk of Citi Being a Value Trap: Very High

Citi is a heartbreaker: It has a long and sordid history of dashing great expectations.

The last time I wrote about Citi was in December 2016. The article posed this question: "Does Citi Deserve to Sell Under Tangible Book Value?"

My answer was "yes."

I provided as evidence the chart below. It shows that investors discount bank valuations based on historical stock price volatility. The greater the historical volatility, the greater the discount. Citi was and is the most discounted big bank because its stock price is the least predictable historically.

If the chart went back 40 years, not just 20, Citi's volatility would be even more pronounced.

Unfortunately, Citi deserves its low valuation and will not, in my judgment, gain parity with peers any time soon given its latest travails.

Chart 3