Summary

- BNY Mellon has a resilient business model based on fee driven revenues that allowed the company to only see a 1% reduction in revenue during Q3 2020.

- At 8.2x TTM P/E and a PEG (EPS) ratio of only 1.0x, BNY Mellon looks like an attractive value investment, trading much cheaper than peers.

- Combining BNY Mellon's current 3.4% dividend yield with the 3.1% average share repurchase rate over the past 10 years brings total shareholder yields up to 6.5%.

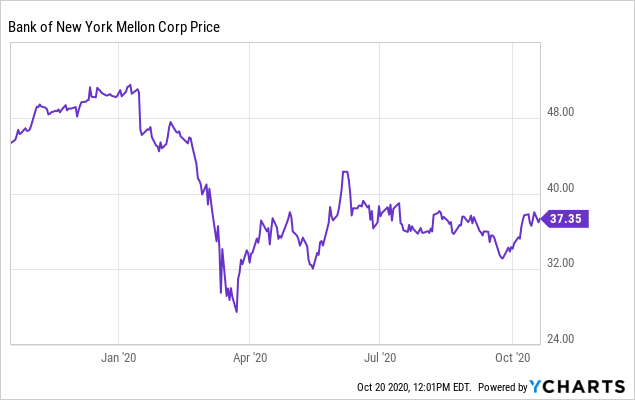

The resiliency of Bank of New York Mellon (BK) in a low interest rate environment leaves the business looking like a great value investment sitting at an 8.2x trailing-twelve month P/E ratio and 0.85x book value. The majority of BNY Mellon's revenue (81%) is earned from fee income with net interest income making up a much less significant portion (18%). This resiliency was evident when BNY Mellon reported Q3 2020 operating results on October 16th which showed total revenue decreased less than 1% with EPS down 8%. This small decrease in revenue and EPS looks out of line with the steep decline in share price and opens up a good entry opportunity for value investors.

Data by YCharts

Data by YChartsA Profitable & Growing Company

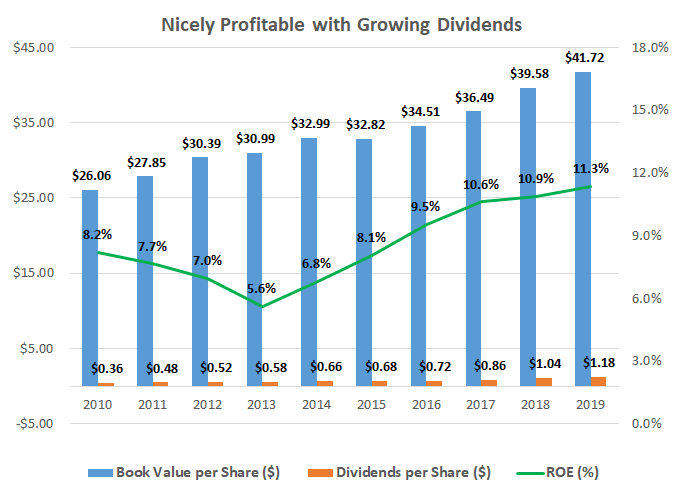

BNY Mellon's strong service offerings have allowed the company to achieve an average return on equity (ROE) of 8.6% over the past decade. While this level of profitability is below my rule of thumb of 15% ROE, in my opinion, the company is able to maintain and continue to increase its intrinsic value over a business cycle as witnessed by its rising book value per share. As I will discuss later in this article, even a business with a mediocre ROE can still make a great investment at the right price.

Source data from Morningstar

Source data from Morningstar