Summary

- Its better than average earnings profile should produce strong profitability metrics for the foreseeable future.

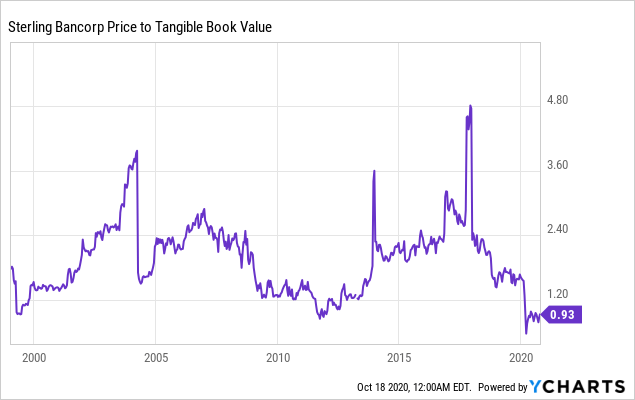

- The current valuation is near multi-decade lows, setting the stage for significant upside potential.

- The credit profile looks solid and significantly better than what the share price is otherwise indicating.

Investment Thesis

Headquartered in Montebello, New York, Sterling Bancorp (STL) is a $30.8 billion asset holding company and parent to Sterling National Bank. Sterling hangs its hat on being able to offer complete solutions to every client no matter the complexity or relationship size. While most banks its size have a wide-ranging footprint, STL only has 80 branches located throughout the New York City and Long Island areas, not to mention the Stony Point and Goshen areas (which are technically a little upstate from NYC).

Sterling also has a pretty diverse loan portfolio. The traditional lending categories like Commercial and Industrial, Commercial Real Estate, and Multi-Family, which make up 16.7%, 28.9%, and 22.8% respectively (total of 68%). After that there are some more "exotic” lending that makes up the remaining balances. Riskier items like equipment finance and asset-backed lending also make up a total of 12.6% of the portfolio.

While I do not think STL has gone over the top in terms of adding risk, I do feel like any potential investors should be made aware of these typically more risky loan categories. However, these riskier loans typically do have better yields and carry higher returns.

When it comes to STL, I am bullish on the stock but only when it comes to the long term. I would not recommend this bank to anyone thinking to hold it for just 6 to 12 months. That said, STL does have a strong earnings profile and on a relative basis appears to be very cheap, near all-time lows on a price to tangible book value per share valuation.

I think the earnings potential is better than average, which should more than support positive earnings growth in the coming quarters. With that being said, I believe the current credit profile appears to be pretty solid, but it's hard to have a large amount of faith since this recession's length is unknown and the past recession was rather tough on the bank. While the bank has changed over the past decade, some above-average turbulence might be felt if this recession is drawn out. If you are looking to invest for the long haul, I would suggest averaging into the shares today.

Data by YCharts

Data by YCharts