Summary

- As BlackRock scales 52-week highs, long-term investors should be inclined to hang on to, even at 23.3x TTM P/E.

- BlackRock's 23.3x TTM P/E ratio and 4.3% earnings yield can be made up for by the high historic growth rates or even a more conservative sustainable growth rate as calculated.

- Revenue per share has grown at an average annual rate of 8.1% over the past decade and EPS has grown by 10.5% annually.

- A sustainable growth rate can be calculated at a lower 5.6% but might not be too relevant for an asset-light business such as BlackRock.

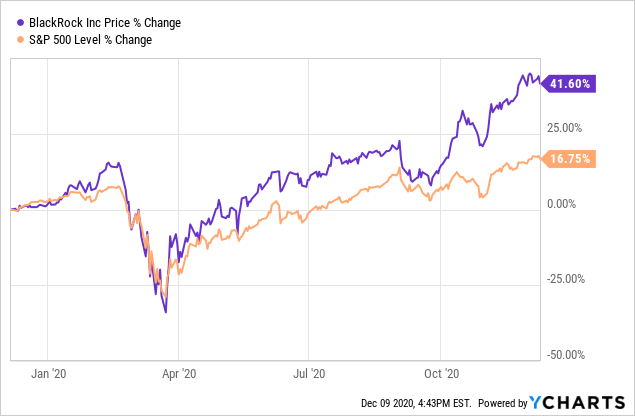

As BlackRock (BLK) scales 52-week highs, long-term investors should be inclined to hang on to, even at 23.3x TTM P/E. BlackRock was one of the companies I wrote about back in March 2020 as markets tumbled and one I was buying with both hands. As markets now reach new highs, BlackRock will be a name that I hold on to as the company still represents good value and growth at a reasonable price. This article will take a look at BlackRock's business and profitability as we add on various growth rates to the current valuation in order to get a sense of potential long-term shareholder returns.

Data by YCharts

Data by YChartsAn Intro to the Company

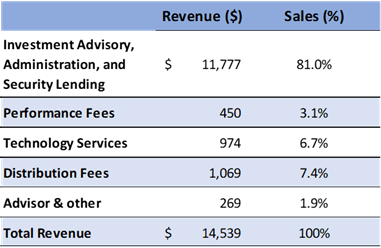

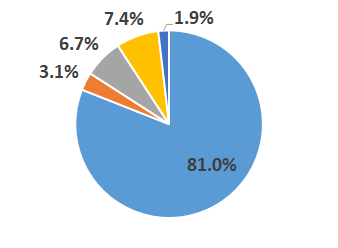

BlackRock is the largest asset manager in the world and collects revenue from administration fees, performance fees, investment advisory fees, security lending fees, distribution fees, and technology service revenues. Base fees earned on assets under management [AUM] make up the large majority of revenues at 81% for 2019, but this segment has a somewhat diversified client base within it. Breaking down AUM fees, BlackRock's popular iShares ETF products made up only 30% of AUM fees in 2019 with Retail and Institutional AUM making up the bulk of the rest.

|  |

Sourced from 2019 financial statements

Latest Results Showing Strength

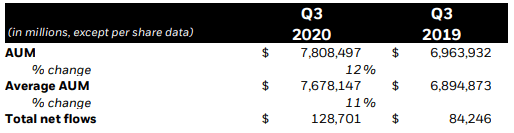

BlackRock's latest Q3 2020 results show continued strength in a unique economic environment. The company reported a strong 18% increase in revenues and a 17% increase in operating income compared to prior year Q3 2019 results. Diluted EPS increased by 24% (or 29% based on adjusted figures) aided by a lower diluted share count in the quarter and higher non-operating income. In terms of the all-important AUM figure, BlackRock's average AUM increased 11% since Q3 2019. Stripping out the increase in broad market valuations, we can look just at the net inflow figure which was $129 billion for Q3 and represents a 9% annualized growth rate in AUM as stated by management.

Sourced from Q3 2020 earnings release

A Highly Profitable and Growing Company

BlackRock's position as the largest global asset manager with a diverse product offering has allowed the company to generate superior returns. While the company is cyclical along with the stock market due to it earning fees on AUM, operations have consistently remained profitable over the past 12 years, including the financial crisis. Since 2008, the company has achieved an average return on equity [ROE] and return on invested capital [ROIC] of 10.3% and 8.9% respectively. This level of profitability is below my rule of thumb of 15% ROE but right at my more important unleveraged ROIC rule of thumb of 9%. The close approximation of ROE to ROIC is an indication of BlackRock's low financial leverage. These return figures allow me to be confident that, in my opinion, the company is able to maintain and continue to increase its intrinsic value in the future.