Summary

- Estée Lauder's lofty valuation is already pricing in a sustainable tailwind for its skin care business.

- Due to lack of competition, high-quality names in the cosmetics space have become too expensive, even after accounting for profitability.

- Intensifying competition brings in additional risk for profitability and top-line growth going forward.

Source: elcompanies.com

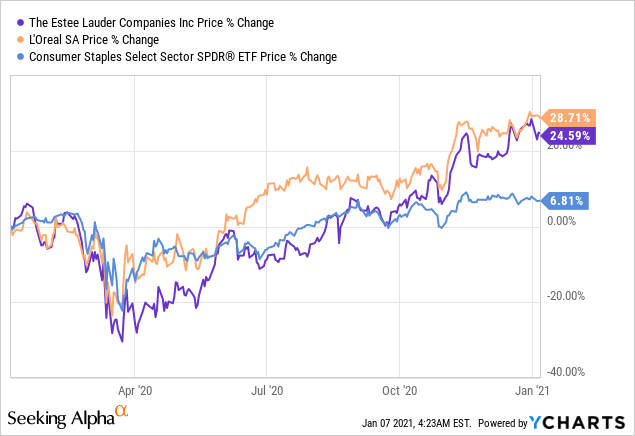

Contrary to the drop in demand of makeup and other beauty products due to the pandemic, 2020 was one of the best years for the high-quality names in the Cosmetics industry, such as Estée Lauder (NYSE:EL) and L'Oréal (OTCPK:LRLCY).

Data by YCharts

Data by YChartsIn the case of Estée Lauder, this outstanding performance in the face of struggling beauty segments like makeup and fragrances came as a result of two major factors. On one hand, the company's strong positioning in skin care, which benefited during the pandemic, and on the other hand, less competition in the space.