Summary

- WPC is a large triple net lease REIT with a high dividend yield and respectable coverage. It will be an appealing choice for most dividend growth investors.

- WPC’s rent collections have remained strong, running at 98% for August. Strengthening collections throughout the sector are helping to boost share prices.

- The REIT has extensive diversification throughout its portfolio and less retail exposure than most triple net lease REIT peers. It also has more industrial properties than most peers.

- WPC delivered more than two decades of consecutive dividend growth for long-term shareholders and strong total returns as well. However, recent prices look quite reasonable.

- Low interest rates are favorable for triple net lease REITs because higher Treasury prices often drive higher share prices. These REITs look to grow often by issuing new equity about NAV and acquiring more properties.

- Looking for a portfolio of ideas like this one? Members of The REIT Forum get exclusive access to our model portfolio. Get started today »

W.P. Carey (WPC) is one of the largest and best triple net lease REITs. This is a solid choice for most buy-and-hold investors. Shares carry a risk rating of 2 and a dividend yield just over 6%. There are a few things you’ll want to know about WPC before we get started:

- They are an international REIT with significant exposure to Western Europe.

- They are able to use their European exposure to issue lower-cost debt.

- They significantly reduced their overall leverage during the last year, which resulted in reducing their risk rating from 2.5 to 2.0 over last winter.

- The portfolio includes an emphasis on industrial and warehouse assets. Pricing in industrial REITs demonstrates the demand for these assets.

- A strategic merger in 2018 simplified the company and made it significantly more appealing.

- Triple net lease REITs usually trade above NAV (net asset value). They issue shares using the premium to NAV. They purchase more properties with the cash raised from issuing shares. These transactions are regularly accretive to existing shareholders.

Layout

We’re going to start with the most current factors. Things that are particularly relevant as of Sept. 9, 2020. These factors will focus on valuation and recent developments. Then we’ll go into a much deeper look at the REIT.

Current Factors - Valuation to Peers

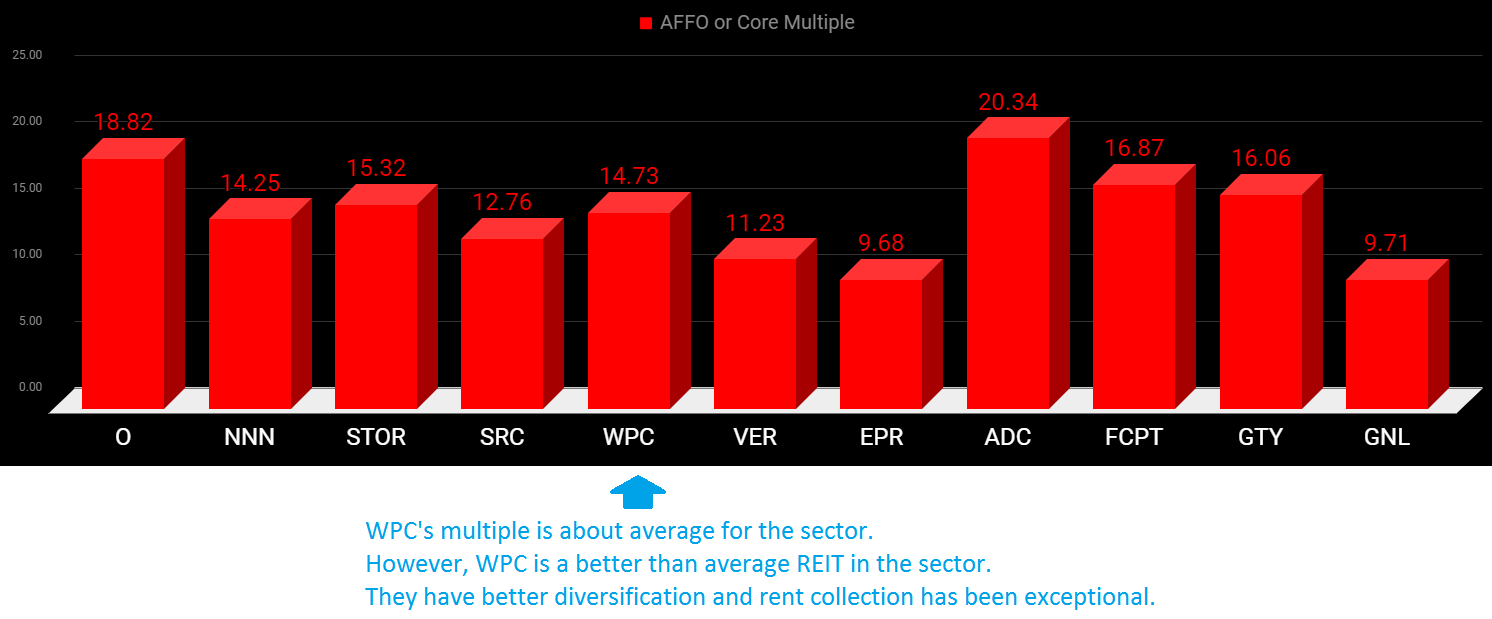

We’re starting with the valuation. We compare WPC with the other triple net lease REITs when evaluating the multiple on analyst AFFO.

Source: The REIT Forum

WPC’s multiple is about average for the sector, but they are better than average. Therefore, it seems WPC should get a higher than average multiple.

Current Factors - Treasury Rates

Treasury prices often have a significant impact on triple net lease REIT prices. Investors treat them as a substitute for bonds, so when Treasury yields go down (Treasury prices go up), the triple net lease REIT yields go down (share prices go up). It isn’t signaling a change in the dividend rate, it's simply a change in valuation. The best-case scenario for triple net lease REITs is a prolonged period of low-interest rates, so long as they don’t have an overwhelming volume of tenants going out of business. Interest rates are currently still extremely low, which bodes well for the sector. However, many retail tenants in the sector (not in WPC’s portfolio) are struggling to pay rent.