Summary

- Quaker Chemical is digesting the acquisition of Houghton, which it acquired at 12X EBITDA and 8.2 times the post-synergy EBITDA.

- It will take three years before the acquisition is fully integrated in Quaker's corporate structure.

- Quaker hiked its synergy expectations from $45M per year to $60M per year, making the acquisition even more appealing.

- The current debt ratio is quite high, but Quaker plans to rapidly reduce its net debt (while increasing the EBITDA).

- Looking for a helping hand in the market? Members of European Small-Cap Ideas get exclusive ideas and guidance to navigate any climate. Get started today »

Introduction

It has been almost a year since I last discussed Quaker Chemical (KWR) and a lot has changed since, as the company has completed the acquisition of Houghton in a cash and share transaction. This deal has the potential to change Quaker’s scope overnight, but this comes with some balance sheet constraints as the company’s net debt has increased due to the deal.

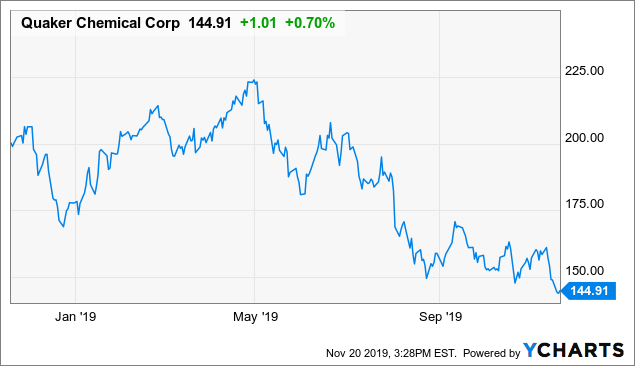

Data by YCharts

Data by YChartsThe acquisition has now been completed

Although the transaction was announced in April 2017, it took Quaker a while to close the deal, and since Aug. 1, the Houghton division has officially been included in the Quaker Chemical corporate structure, about two years after the originally scheduled closing date of year-end 2017.

Quaker paid just over $170M in cash and issued 4.3 million shares to the sellers of Houghton which currently represents almost a quarter of Quaker’s share count. Additionally, Quaker was required to refinance almost $660M of debt. Quaker was able to draw down $930M (in a combination of a USD and EUR term loan as well as a credit facility) of its new $1.15B credit facility to complete the cash payment as well as the debt refinancing, so the company is all set.

Source: Company presentation

Considering Quaker continues to generate a decent amount of free cash flow (see later), I expect the $180M revolving credit line to be repaid soon. As Quaker received $37M from the sale of the mandatory divesture of a division to Total (TOT), the net cash outflow related to the purchase of Houghton was approximately $135M.

An expensive acquisition as the 4.3 million shares of Quaker that were issued to the seller (the Hinduja Group) have a current value of in excess of $600M, which means the total net payment was around $770M while an additional $660M of net debt had to be refinanced, resulting in an enterprise value of around $1.43B. Considering Houghton had a trailing twelve month EBITDA of $118M, the purchase price of 12 times EBITDA appears to be steep. But before slamming Quaker for acquiring Houghton at an EBITDA multiple of 12, there are two mitigating factors. First of all, the sellers have received a large chunk of shares in Quaker Chemical, and I hope this indicates the Hinduja Group is willing to act as an anchor shareholder.