Summary

- Wells Fargo's consumer banking deep-dive reiterates the cost-cutting theme.

- However, added uncertainty around the expense run-rate adds one too many moving parts.

- Valuing WFC requires investors to ascertain earnings three years out.

- Recent run leaves little multiple upside; moving this to the "too hard" pile.

Wells Fargo (WFC) has had a great run in the second half of the year, but I struggle to see sustained share price outperformance from here; though the appointment of a new CEO adds clarity, discerning the bank's earnings power is difficult at this point, pending clarity around regulatory risk and the expense run rate. To be clear, there is a cost out story emerging here, as last week's consumer banking deep dive laid out. However, this is a three-year story, at least, and I am simply not prepared to value the stock on forward earnings three years out. Taking a leaf out of Buffett's book, I am placing WFC firmly into my "too hard" pile.

Wells Fargo Goes Digital

Wells Fargo's recent Consumer Banking investor meeting was particularly noteworthy, considering it came hot on the heels of the new CEO appointment and featured David Kowach, the new community banking head. For some context, the consumer banking segment, led by Mary Mack, is the critical piece to the Wells Fargo story, contributing the majority (~51%) of revenue in FY18.

Source: Consumer Banking Day Presentation Deck

By and large, the major focus of the slide deck was on automation/digitization across business lines and expanding cross-selling opportunities. The digital transformation will start at the branch-level. While customers' engagement was previously limited to the branch tellers; today, customers who open a Wells Fargo account will also be introduced to WFC's digital offerings by in-branch personnel. WFC benefits from improved efficiency as digitalizing the experience allows them to cut down on the frequency of branch visits, while simultaneously deepening and broadening the extent of the customer relationship. Early efforts have seen good traction, with customer experience survey scores up to three-year highs.

Source: Wells Fargo 3Q19 Presentation Deck

Digital is crucial if management is to shift toward a more advice-driven model and better leverage its data. The overarching aim is to more completely, proactively and efficiently service the Wells Fargo customer to capture a greater wallet share. The untapped potential here is significant, as >50% of Consumer Banking customers use only one service today.

Community Banking Gets a New Head

Community Banking's new head, David Kowach, is focused on refocusing the community bank to advice from transactions - in his prior role as CEO of Wells Fargo Advisors, he oversaw a similar transition from a transaction-based to an advisory-based model.

The overarching aim is to evolve the role of the branch to be more of an advice center, with bankers capable of delivering the whole franchise inclusive of mortgage, student lending, and Wells Fargo Advisors. i.e., addressing the full financial life cycle.

Source: Consumer Banking Day Presentation Deck

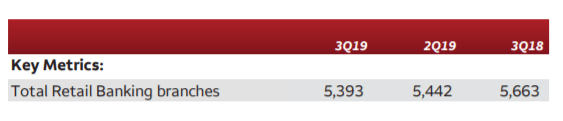

The aim is to rationalize Wells' branch footprint efficiently - branches are down from 6,197 as of 2012 to 5,393 in 3Q19 (13% of total branches) over the past few years, but they have only lost 1% of the customers associated with these rationalized branches.

Source: Wells Fargo 3Q19 Presentation Deck

Further branch-level opportunities lie in shifting to smaller footprint branches and reducing the branch network in smaller markets. Additional initiatives include increased in-branch personnel training to minimize the need for more specialized personnel.