Summary

- With the end of shelter-in-place orders, IQOS PoS commercialisation effort can continue to drive growth.

- Due to IQOS margins being 1.68x traditional cigarette margins, if IQOS becomes adopted elsewhere at similar rates to Japan, overall PMI margins will greatly improve.

- Since most IQOS users are converted smokers of traditional products, the fact that PMI is a first-mover in a winner-take-all dynamic means that substantial market share will be gained.

- According to our model, which takes into account various relevant business concerns like cannibalisation from IQOS growth, we think that a highly conservative scenario is being priced in.

- If IQOS success across geographies is in line with Japan, upside with this stalwart could be as high as 50%, unprecedented for an iconic large-cap like PMI.

In light of the coronavirus pandemic, we were overweight the consumer staples sector with a focus on big tobacco. Besides precedent for resilience of this sector during economic downturns, tobacco shops were also one of the few amenities still available to the public during lockdowns. Furthermore, shelter-in-place orders were a recipe for relapses into the smoking habit, and in the cases of more staunch smokers, we could expect more frequent smoking. Our view was vindicated later by the Philip Morris (NYSE:PM) Q1 earnings call results which showed substantial resilience.

Despite operational resilience, PMI underperformed the overall market. Currently, the company has not taken part in the recent rally despite the fact that Philip Morris is ready to take a lead in the heated tobacco space globally, with their commercialisation efforts for IQOS now ready to slowly resume with shelter-in-place restrictions coming to an end. Although the market potential for IQOS is being recognized by markets, with it growing in a matter of years to be one of the largest tobacco brands in the world, what the market seems to be failing to realise is that there are multiple margin expansion vectors that will result from an emphasis of IQOS products in the PMI sales mix. Moreover, by tapping into the modern smoking culture around vaping, conversion of users of competitor cigarette brands in a winner-take-all heated tobacco dynamic will mean substantial market share gains to offset any secular declines. If IQOS' success is even remotely similar in the rest of the world as it was in its proven market of Japan, we are looking at a potential 50% increase in NOPAT and consequently upside in the upper double digits in the best case scenario. For a company that has superb resilience to COVID-19 in the event of secondary lock-down measures and is a storied market stalwart weathering crises of all types in the past, a double-digit upside presents an exemplary opportunity in an iconic large-cap. To understand the circumstances that can lead to these dramatic revaluations, we first need to understand the market potential of IQOS and hence its ability to influence PMI's profits.

IQOS Emphasis and the Margin Impact

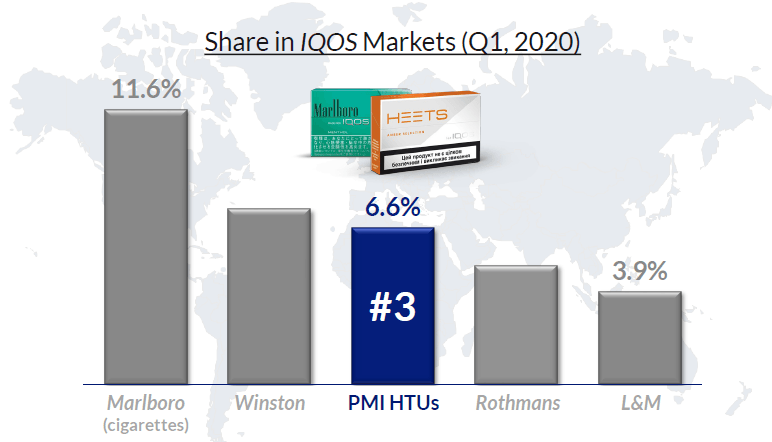

In April 2019, a version of IQOS became the first heat-not-burn product to be authorized for sale by the US FDA under the PMTA pathway. The agency's rigorous two-year review led to the conclusion that IQOS is "appropriate for the protection of public health." More recently, the FDA has approved IQOS marketing as a modified risk product, helping it further substantiate it as a potential reduced risk product with the FDA stamp of 'beneficial to public health' as a smoking alternative. This regulatory success is in contrast to other alternatives to combusatibles, where Menthol-based and flavoured e-cigs are being heavily opposed by regulators and have crippled them from capitalising on the need in the market for a reduced risk alternative to smoking. Indeed, this large void has already started to become filled by IQOS, which due to blinding growth since it was launched in 2015 is already the third largest brand in the world (first in heated tobacco), just after iconic legacy brands like Marlboro and Winston.

(Source: PMI 2020 First-Quarter Results)

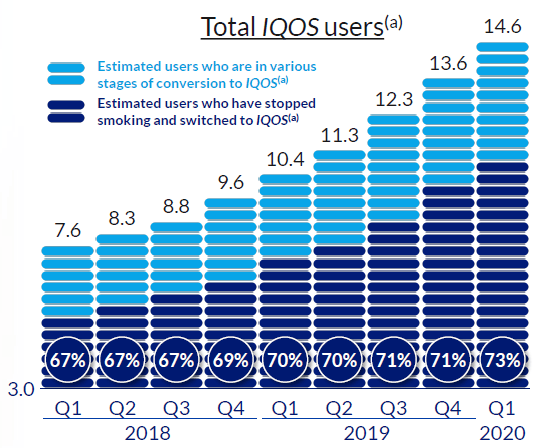

Regarding the smoking market in general, it is predicted that, over the next decade, the number of smokers will remain largely unchanged from the current estimate of 1.1 billion, despite the considerable efforts to discourage smoking. Indeed, the data in markets where IQOS and reduced risk products have gained market share bear this out. Since 2017, combined data for cigarettes and heated tobacco units have barely declined in the EU (excluding Eastern Europe), a far cry from the substantial 5% market decline rates disclosed by big tobacco firms. This indicates that a more stable base of nicotine users, bolstered by the creeping effect of growing 18+ populations, exists where reduced risk products are available. This is substantiated by the fact that approximately 71% of the tens of millions of IQOS users are converts from legacy smoking products.

(Source: PMI 2020 First-Quarter Results, figures in millions)

Even if we rightly acknowledge that IQOS might be cannibalising some users in PMI's legacy brands, IQOS growth will still generate substantial value. This is because there are three ways that IQOS' emphasis in the mix are improving margins that will more than offset any cannibalisation effect. First of all, they sell at a higher margin than traditional products do. Second, as the IQOS segment becomes more emphasized in the mix, the higher material costs involved in shipping traditional products will also be forced downward. The fact that IQOS sales don't have excise taxes levied on them is the final way that their mix contribution increases PMI's margins. The lower excise tax could very well be a durable source of improved profits, as the lower rate isn't a regulatory oversight. It reflects the fact that the company has been largely successful in demonstrating to regulators that NGPs are not cigarettes, and as such, they are generally taxed either as a separate category or as other tobacco products, which typically yields more favourable tax rates than cigarettes. The fact that they didn't get crushed by the regulatory hammer while Menthol-based and flavoured products did is a testament to this effort.