Summary

- After a sharp tech sell-off, Etsy shares are down 25% from the recent all-time high.

- Finally, COVID-19 stocks decelerate to a more reasonable level. We believe it's an excellent time to consider a starter position in Etsy.

- Etsy's recent performance shows great strength in its platform; it grew at triple digits even without COVID-19 items, increased operating leverage, and printed cash at scale.

- Etsy is proving that it is no longer a niche eCommerce site for just handcrafted items, and has now expanded to more retail categories and geographies.

Investment Thesis

We have been wrong before on Etsy (ETSY) and likely to be wrong again. But, after the sharp 25% fall in the share price, Etsy is a buy.

Pre-pandemic, the company was trading at around 30x EV/FCF and 10x EV/Sales and was growing at a 30% rate. Today, Etsy trades at 33x EV/FCF and 11x EV/Sales but grows at triple the rate pre-pandemic, at 100% vs. 30%.

An investment in Etsy today isn't just about a more reasonable valuation; it's a stickier platform with higher profitability and a longer runway for growth.

Impressive growth and no longer a niche handcraft eCommerce site

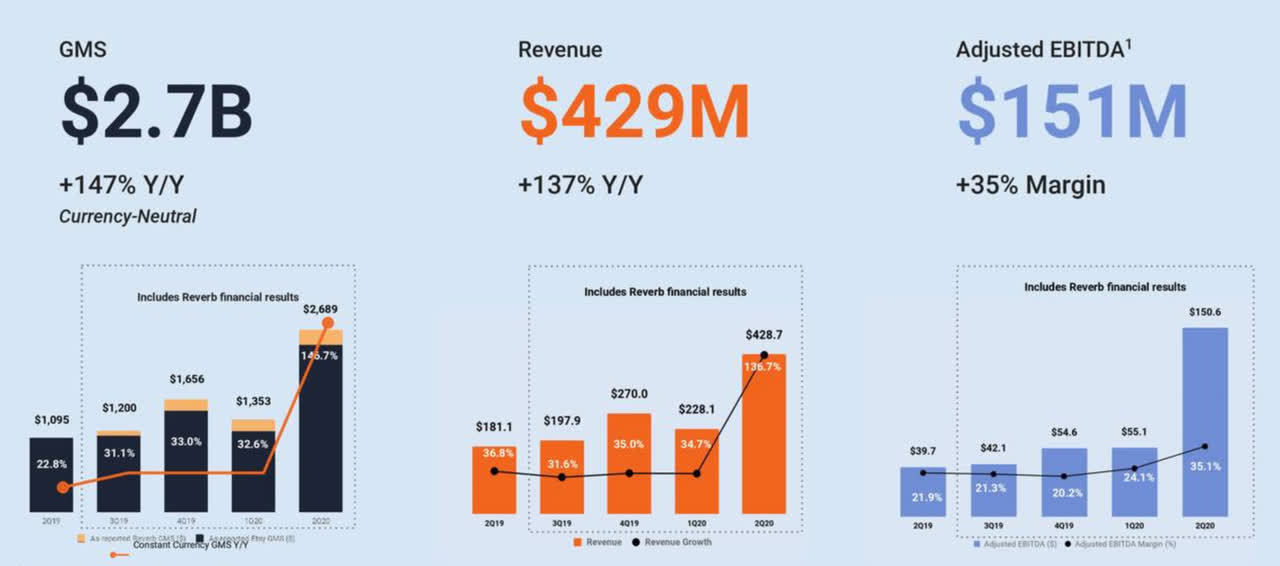

Etsy reported spectacular Q2 2020 results. Gross merchandise sales ('GMS') was up 147%. Active buyers and sellers were up 41% (60.3M) and 35% (3.1M) YoY, respectively. As a result:

- Revenue was $429M, up 137% YoY.

- Gross profit was $317M, up 159% YoY.

- Operating profit was $119M, up 569% YoY, resulting in an operating margin of 28%.

- Net cash provided by operating activities YTD was $250M, up 208% YoY.

All financials benefited from the COVID-19 tailwinds. However, looking at non-mask sales, GMS was up 94%.