Summary

- My target price for AWK is $165, giving investors a possible upside of almost 16% in the next one to two years.

- I estimated that the company's revenue would grow at a CAGR of 4.2% based on the company's guidance and historical revenue growth of each business segment.

- Based on the information in my article, I believe net income will grow at a CAGR of 7.4% during the forecasted period.

American Water Works Company, Inc (AWK) has been my favorite company to analyze. It is one of the few companies that I have covered that I feel is ran by disciplined and focused executives. Besides this, the company's guidance usually is correct, and the profit margins are pretty stable. I will present my revenue estimates from my last AWK article and my updated DDM Valuation in this article.

Important Information And Key Assumptions From Original Article

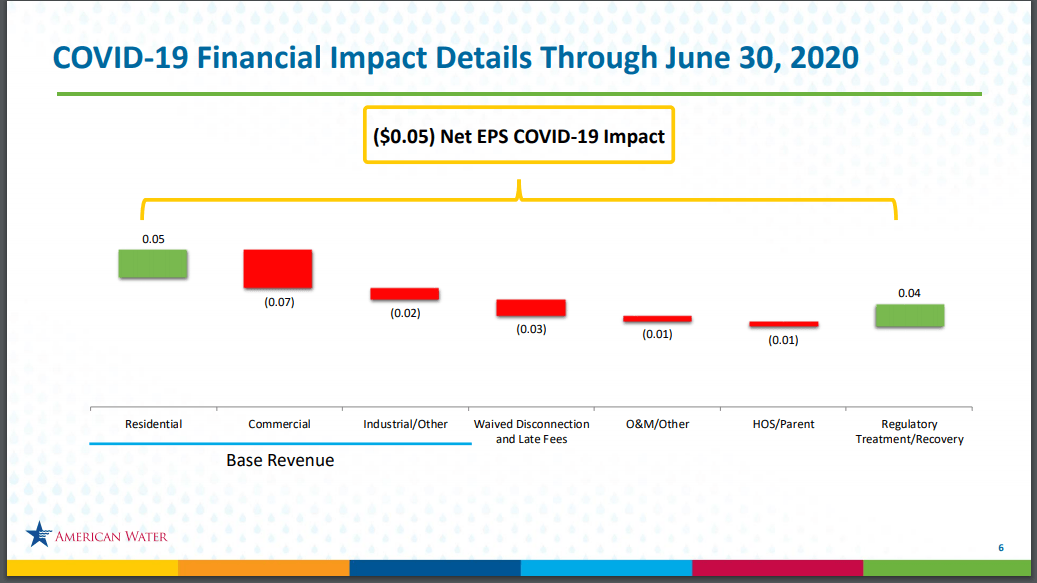

In part one of this series, I mentioned how I was shocked that AWK lost $21 million (after-tax loss of $15 mn or $ 0.09 in EPS) due to the adverse effects of the coronavirus. I expected that the company would lose a couple of million because of the increase in delinquent accounts. Yet, I didn't take into account that commercial/industrial loss in revenue would outweigh the growth in residential revenue.

Figure 1 - Impact of COVID 19 On H1 2020 EPS

Source: Q2 2020 Results Presentation

Source: Q2 2020 Results Presentation

As seen in figure 1, the growth in residential revenue increased the company's EPS by only $ 0.05. The decrease in commercial and industrial revenues decreased the company's EPS by $ 0.09. In my original estimates I felt that residential revenue growth would balance out the decline commercial revenue.

In my last article, I estimated that the company's revenue would grow at a CAGR of 4.2%. This growth rate is based on the company's guidance and historical revenue growth of each business segment as I will further detail below.