Summary

- Verint Systems gears up for the spin-off of its Cyber Intelligence unit, Cognyte.

- As the FY22 guide illustrates, both the Customer Engagement and Cyber Intelligence segments are on track for more predictable, high-margin earnings streams.

- Given best-in-class comp Palantir commands ~50x EV/Revenue, the implied ~1x EV/Revenue multiple for Cognyte at current levels skews the risk/reward favorably.

With the spin-off of its Cyber Intelligence unit on the way, Verint Systems (VRNT) looks set for a valuation boost. Recently IPO’d Palantir (PLTR) shines the spotlight on the value-unlocking opportunity - given the many similarities between the spinco and PLTR, there is a good case, in my view, for a significant re-rating from the implied ~1x EV/Sales multiple it currently commands within VRNT. The next steps include a 20F filing, as well as an investor day early next year, both of which will offer more color on the separation. With improving trends across both businesses, an undemanding multiple, and a separation catalyst on the way, VRNT offers investors a highly favorable risk/reward.

FY22 Guidance Offers a Look into Verint Post-Spin

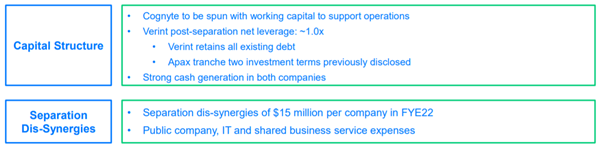

Management has been making all the right noises on the planned separation so far, and the level of disclosures offered on the recent quarterly call was more of the same. Not everything is finalized, though, as the FY22 guidance showed - the company is still guiding both segments, Customer Engagement and Cyber Intelligence (Cognyte) as if the two were operating under the same entity. But come January, and soon after end-FY21, both businesses will split into individual public companies. Management did offer some new insight into the Cognyte spin-off, though, citing ~$15m of dis-synergies per company in FY22 and a higher leverage on each business (spinco and remainco) post-spin.

Source: Investor Presentation

Cloud-Driven Growth at Remainco

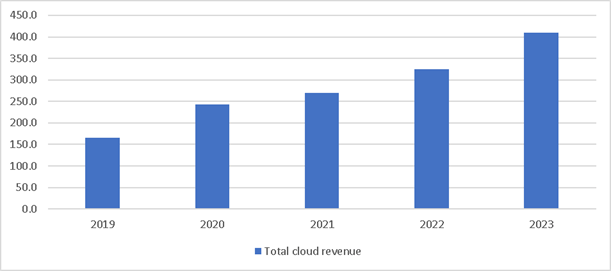

Remainco, i.e., the retained Customer Engagement business, is on track to hit its ~$1bn revenue target by F24, which implies a solid mid-to-high single-digit % CAGR. The quality, though, is the key highlight – the revenue base will shift to ~90% recurring on an accelerated ~30% CAGR in the cloud, with two-thirds of software bookings from SaaS. Not only does this represent a step-up in its strategic shift, but it also comes with much-improved economics, underpinning further margin expansion post-separation.

Source: Company Filings, Author’s Est

Broadening the Recurring Revenue Base at Spinco

The FY22 guide for the spinco, Cognyte, was also bullish, with growth expected to hit ~10% in FY22 before accelerating further in FY23-24. This bodes well for the segment’s valuation multiple, even ahead of the separation. Plus, there’s also the improving profitability to factor in - VRNT has ample room to improve margins via the growing “recurring” revenue portions of the business, which has grown from 55% to 70% in recent years. The broader recurring revenue base has translated into stronger gross margins, which were up 500bps in the most recent quarter. With the acceleration that began in the higher-margin recurring revenue strategy now a permanent driver for the segment, I see ample runway for further margin expansion in FY22/23 after lapping the post-spin dis-synergies in FY22.